Global Semiconductor Supply Chain

I recently shared a piece on the semiconductor industry, providing a basic introduction of what this industry is all about and throwing light on the key players, namely the 1) equipment makers, 2) the foundries/IDMs and 3) fabless design companies.

The second part of that article highlighted 5 small-cap semiconductor companies that are flying under the radar which have been the best semiconductor companies in terms of their price performances YTD.

I like to follow up on the first semiconductor article with a more in-depth breakdown and review of this industry that is powering our digital economy. Yes, semiconductors have become our “digital oil”. Where might the opportunities be in the semiconductor industry in the coming decade?

How Big Is The Semiconductor Supply Chain?

According to data from Statista, semiconductor sales have grown from $33bn back in 1987 to a projected $573bn in 2022.

The semiconductor supply chain is made up of thousands of players but can be categorized into four basic segments:

- Design

- Fabrication

- Assembly/Packaging/Testing

- Equipment manufacturer

Design

The first step in the creation of an integrated circuit is to design it and this task is typically undertaken by the “fabless” companies such as Nvidia, AMD, etc which focus on the “software” component of the chip production process.

A massive amount of R&D is spent annually by these fabless companies to design chips for a particular niche segment, for example, gaming, PC. These fabless companies will then look to outsource the fabrication work of these chips that they have designed to foundries.

Fabrication

The fabrication work is done by foundries who convert the design into physical production, in this case, a chip. This will involve the usage of different raw materials starting with silicon to transfer the circuit design into its physical wafer form.

Assembly/Packaging/Testing

The fabrication process will typically result in a “wafer” that has been printed with several hundred individual integrated circuits. The next step is to dice them into die, test and package them for end-users.

Manufacturing equipment

All of the above can only be executed and automated with machines and equipment that are provided by the equipment manufacturers.

There are some companies with can do multiple functions, such as both design and fabrication of their chips. These are your integrated device manufacturer or IDM for short. Intel is an example of an IDM, a company that is capable of designing, fabricating and packaging its chips.

However, Intel is receiving a “lot of heat” because its fabrication process is seriously lagging behind that of TSMC, the undisputed market leader in the arena of fabrication. Most companies have now adopted a strategy to focus on what they do best (design, fabrication, testing, etc) instead of being an integrated player.

For example, AMD which was once an IDM, split into a fabless company, retaining the name AMD while its fabrication arm is now known as GlobalFoundries.

Which Of The Above Segment Is The Most Important?

According to the Boston Consulting Group and the Semiconductor Industry Association in a research report published back in April 2021, the DESIGN portion of the value chain is the area that provides the greatest “value add” to the whole semiconductor industry.

What does value add mean over here? Assuming that the processor chip in your smart phone costs $50 to produce, how much of that $50 is attributed to the design of the chip, how much to fabrication, how much to testing and packaging, etc.

The design portion accounts for the largest R&D cost as well as the greatest value add for the semiconductor industry, coming in at 53% and 50% respectively, according to the BCG report. Chip design companies such as Nvidia etc spend a significantly large portion on their R&D expenses, while actual Capex cost might not be that substantial. They can then charge a “premium” for the chips that they design.

On the other hand, fabrication companies like TSMC spend the bulk of their expenses on Capex, mainly purchasing equipment required for the fabrication process. Their service accounts for approx. 24% in the cost of a processor chip.

Now let us take a look at who are the major companies in the respective segments.

Who Is Leading The Semiconductor Industry?

The diagram above illustrates some of the major players in the respective segments of the semiconductor supply chain. Do note that the list above is not exhaustive.

There are still many IDMs around, the bigger ones being Intel, Samsung and Micron. Again, IDMs are companies that design and manufacture their chips, although there has been a recent trend of certain IDMs relying on foundries to fabricate their chips and Outsourced Assembly And Test (OSAT) companies to do a portion of their assembly, packaging and testing requirements.

Major fabless design companies are the likes of Qualcomm, Nvidia, Broadcom, AMD and Mediatek. These are the companies that generate the greatest value add in terms of the entire chip production through their chip design.

You also have your foundries which are typically independent parties that focus on chip fabrication work for fabless companies. The largest players are TSMC, Samsung, UMC, GlobalFoundries and SMIC.

You have your assembly, testing and packaging companies that account for a relatively small proportion of the semiconductor industry in terms of sales of value add. Some major companies are the likes of ASE, Amkor, Powertech, etc.

A key area that is not highlighted in the above diagram is the equipment manufacturers. The entire semiconductor production involves more than 50 types of sophisticated specialized equipment as can be seen from the diagram below.

Some of the largest players when it comes to semiconductor equipment manufacturing are the likes of your ASML, AMAT, Lam Research, KLA, etc.

Design Dominates

I have earlier highlighted that the Design “Fabless” segment is the area that provides the greatest value add, according to research done by BCG. It is worth highlighting that within this key area, two ancillary segments are critical:

- Electronic Design Automation, and

- Core Intellectual Property

These are the supporting players that are the driving forces behind the Design companies. While the overall value add to the semiconductor industry is pretty marginal at just 4%, without the contribution of these companies to automate the design process, design companies will not be able to accomplish their task efficiently.

Electronic Design Automation

Electronic Design Automation, like what its name suggests, is a suite of software tools to automate the design process and to better manage the scale and complexity of the entire chip design process.

Some of the major players that are less well known compared to their fabless counterparts are the likes of Cadence, Synopsys and Ansys, all of which are EDA companies whose products are critical to the success of the development process.

Core IP

Not many people of heard of the term Core IP or know what it represents. One would probably have heard of the company ARM, which is currently pending an acquisition by Nvidia which is a deal worth $40bn back when it was announced in Sep 2020 but that valuation has ballooned north of $50bn, following Nvidia’s market cap increment.

ARM does not fall within the 4 categories highlighted earlier. While it is a design company, it does not design chips. It develops and sells blocks of intellectual property that chip design companies like Nvidia and Intel can build upon to create their IC products.

The company monopolizes the architectures for processors used in mass-market products such as mobile phones, smartwatches, tablets, smart TVs, etc. Today, ARM claims to have 200bn ARM-based chips being shipped in 2021.

That is a massive number of ARM-based chips and that market continues to grow as we move into an era of the internet of things where ARM technology will have a huge advantage due to its “edge” presence.

In summary, these two ancillary segments, EDA and Core IP are companies that allow design players to do what they do. Without these players and their products, design companies will not be able to function as efficiently as what they have been able to do.

Strong Demand For Fabrication

While design companies provide the greatest value add in the entire semiconductor supply chain, it is the demand for fabrication capacity that is sky-rocketing at present. This is due to two main reasons in my view:

First, beyond the current supply bottleneck for chips, as evident in the automotive industry, driven in large part by COVID-19, the world is getting increasingly digitalized with major themes such as 5G and IoT set to take center-stage in the current decade. That will significantly bolster the demand for chips to be used in all-things electronics.

Second, there is an ongoing effort by several countries to aggressively pursue national semiconductor independence, a trend that is creating new hubs of microelectronic development.

For example, while the US is home to many design companies and accounts for 29-74% of design software, they currently only make up for approx. 12% of the wafer fabrication (silicon), with Taiwan and South Korea accounting for the lion’s share through TSMC and Samsung respectively. This has prompted the US Senate to approve a bill that would provide $52bn to subsidize chip fabrication in the US.

Big foundries/IDMs are now incentivized to “set up shop” in the US, with TSMC, Samsung and Intel all announcing big Capex plans to build cutting-edge fabrication plants in the US.

According to this data by the US Semiconductor Industry Association, a $50bn incentive program by the US government could result in 19 new fabrication plants being built onshore, with the US now accounting for 41% of the fabrication capacity.

The same thing is happening in China where wafer fabrication accounts for 16% of total global demand but is expected to increase to 20% over the coming years.

In a nutshell, demand for fabrication facilities will likely take center stage in the coming years as both the US and China aim to achieve semiconductor independence. It is likely that the US is currently ahead of the game in terms of achieving that independence, considering that it has dominant control over the “design stage” of the production process, an area in which China is seriously lagging.

Semiconductor Industry Opportunities

1. Foundries

It is unclear if the current chip shortage is a transitory one or a more permanent issue that will drag beyond the coming 2 years. Foundries currently enjoy strong pricing power, particularly for those who can meet the demand for complex chips, such as TSMC.

However, the longer-term trend could be one where the current massive investments in fabrication facilities will result in an oversupply of chip capacity that will drive down product prices for foundries. Concurrently, heavy investment in Capex will be required by these entities over the coming decade.

There are now only a handful of companies with 5nm fabrication capabilities. Samsung is likely the only company with 5nm capability for both logic and memory chips.

2. Equipment Manufacturers

Equipment manufacturers are also current beneficiaries of elevated Capex by foundries and IDMs, with the strong demand for fabrication facilities implying that demand for semiconductor equipment will also be extremely robust over the coming years.

Equipment manufacturers such as ASML which has a dominant market position in photolithography equipment are strong beneficiaries of the rise in demand for fabrication facilities which implicitly implies that demand for its equipment will also witness strong demand.

Take, for example, advanced lithography equipment which ASML supplies, specifically those that harness Extreme Ultra-Violet (EUV) technology are required to manufacture chips at 7 nanometers and below. One such machine alone can cost $150m.

3. Design Companies

Design companies that manufacture chips used in certain mega themes such as Autonomous vehicles, 5G, AI and IoT will stand to benefit from the rise in demand for such services and products.

For example, to play the autonomous vehicle trend, investors might want to take a closer look at NXP Semi which is the largest automotive chip provider, accounting for about 11% of the market.

The largest fabless design companies currently are Qualcomm, Broadcom and Nvidia and these companies all have operations that are exposed to these growing mega themes.

Smaller market cap companies such as Cadence and Synopsis that are exposed to the EDA segment will also be likely beneficiaries, tapping on the growth of chip design companies.

However, it will be interesting to note if the current chip shortage situation will result in a margin squeeze ahead for these fabless companies who are dependant on foundries to manufacture chips for them. This might happen if they are not able to pass on the costs to their customers.

For example, TSMC plans to raise its product prices by 10-20% in 2022 and this will have an impact on its design customers such as Mediatek, Qualcomm and others if they are not able to pass on the price increase to their customers.

Quick Look At The Charts

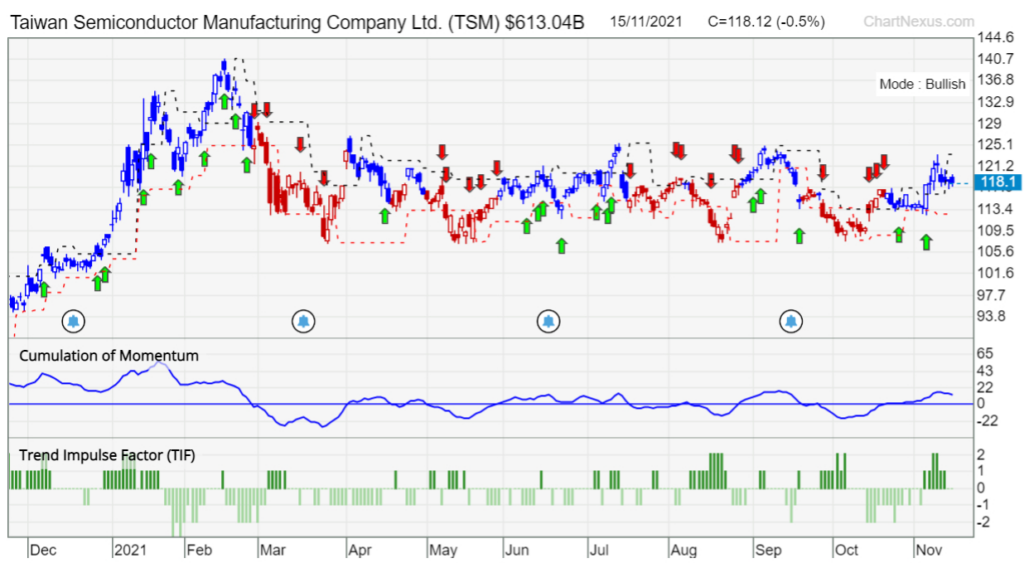

Of the many companies mentioned above, let’s just take a look at one which has not yet been featured from the last few articles – TSMC:

According to the chart on TradersGPS, TSM has been trending sideways for most of this past year. If you may notice, however, there was a strong upward move from December to mid-February.

The picture will be more holistic if you zoom out further to see that the upward trend began even before what you see here in December. This current sideways trend can therefore be interpreted as a “digesting” of this move, like a consolidation phase.

While this would not be an ideal trading candidate for a position daily strategy, there was indeed a signal given off earlier this month. It remains to be see if TSM is finally breaking out, or if it would continue trending in this range between $109.50-$125.10.

Conclusion: Semiconductor Industry Outlook

There are opportunities aplenty in the semiconductor industry, one which is relatively volatile, with short-term headwinds in the form of chip shortages. This might benefit chip makers aka foundries that have pricing power while fabless design companies that depend on the former to fabricate their chips could be at the receiving end.

Long-term commitments by foundries to expand their production capability bodes well for equipment manufacturers which will likely witness a stream of steady demand for their products over the coming decade.

Other notable players in the semiconductor supply chain that could stand to benefit from the rise in demand for semiconductor products is EDA players and Core IP entities (which ARM has a monopoly in this arena).

If you enjoyed reading this article and various other investment + personal finance articles, do visit New Academy of Finance. Royston has more than 10 years of buy and sell side experience as a financial analyst. He constantly posts interesting, valuable and actionable articles.

If you’d like to get a FREE e-course and learn how to better time your trade entries, click the banner below: